What Is a Chart of Accounts (COA)? | How to Structure Your COA | Segmenting Your Financial Reports | Revenue Recognition

During the first four chapters of our Playbook, we focused on building the finance and accounting infrastructure necessary to create scalability within your organization. We focused on how things are done traditionally and issues many firms experience, the essential team members within an F&A department, their roles, and the technology systems necessary to create visibility and scalability in operating. Accurate data is the key to accurate reporting.

That’s quite a bit about inputs. What about the outputs? The ultimate goal is to create accurate, actionable financial reports that will guide strategic decisions. With the ultimate “output” goal being actionable financial reports and KPI development, it all starts with your Chart of Accounts. The Chart of Accounts is the key building block to quality reporting capabilities, so it’s an ideal starting point.

What Is a Chart of Accounts (COA)?

A COA is an index of all the financial accounts in the general ledger. The accounts are divided into categories and sub-categories and ultimately serve as the foundation for your financial statements. Structuring your COA appropriately gives you clarity by providing insights into your financial statements and company performance.

Your COA should be broken down into five sections. Some sections correspond to your company’s Balance Sheet and some sections to your Income Statement:

- Balance Sheet: Assets, Liabilities, and Equity Accounts

- Income Statement: Revenue and Expenses

One way to understand what a COA is and how it works is to think of a storage facility full of shelving units. Each shelf has several storage bins on it. In a storage facility, those bins might hold supplies or equipment. In the case of a COA, a “storage bin” is a specific account, and the “bin” is full of the transactions related to that account. The “shelving unit” might be the overall category.

For example, your COA might have a category (or “shelving unit”) for Client Invoices you need to pay. The Vendor Invoice category is considered a Balance Sheet category since your business needs to pay those invoices. It’s a liability. On the Client Invoices shelving unit, you’ll find several bins, one for each client that has sent you a bill you need to pay.

Some of the sub-categories in the liability category that fall under the Balance Sheet umbrella include:

- Accounts payable.

- Payroll liabilities and taxes.

- Invoices payable.

- Credit card payments

Sub-categories under the assets category on the Balance Sheet side of your COA include:

- Buildings your company owns.

- Vehicles your company owns.

- Cash.

- Bank and investment accounts.

- Trademarks and patents.

Under the equity accounts category on the Balance Sheet of the COA, you might have the sub-categories such as:

- Retained earnings.

- Preferred stock.

- Common stock.

Over on the Income Statement side of your COA, you might have a “shelving unit” for Accounts Receivable. Each client you’ve invoiced would have its own “bin,” and that bin would contain a list of the invoices you’ve sent. Other sub-categories in the Revenue category on the Income Statement side of the COA include:

- Rent received.

- Income from goods sold.

- Income from services rendered.

The Expense category falls under the Income Statement when the expenses are necessary for generating revenue. Some sub-categories include:

- Utilities.

- Rent paid.

- Equipment purchased.

- Cost of goods sold.

- Depreciation.

If a storage facility doesn’t have clearly labeled bins or shelving units, it becomes difficult, if not impossible, to find what you need. You might spend hours looking for a particular part or piece of equipment. The same is true for your accounts. If your COA isn’t organized and arranged, you might miss certain expenses or wonder why your company’s spending is so high in one category. A well-organized COA lets you see how each account affects your business, so you can make financial decisions accordingly.

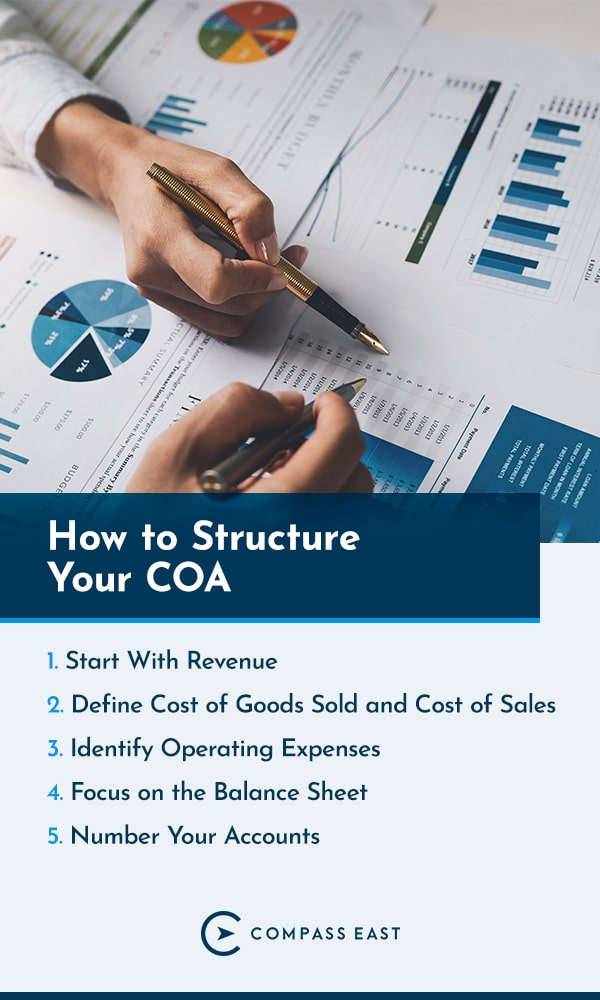

How to Structure Your COA

You can take several approaches when structuring your COA. One option is to get extremely complicated and granular. However, it’s often easier for non-accountants to think conceptually first. Think back to the storage facility example and consider how many shelving units (categories) and bins (accounts) you’ll need. For example, you might need a shelving unit for Revenue, one for Expenses, and one for the Balance Sheet.

Draw a flowchart that groups your accounts logically. You can assign a number to each account later. Consider these steps to learn more about how you can develop your COA.

1. Start With Revenue

It helps to start at the beginning of your organization process with the category that is likely the most understandable — how your business makes money. Create a category for operating revenue or the primary ways your company brings in income.

Under the Operating Revenue category, create sub-categories for each revenue stream and sales accounts, discounts and returns. Some of the “bins” you might make in this category include:

- Revenue stream 1, which may include goods sold.

- Revenue stream 2 might include subscriptions.

- Revenue stream 3, which may consist of add-on services purchased, such as an extended warranty.

- Sales account.

- Sales discount.

- Sales allowances and returns.

Depending on what your company does, it might have two forms of operating revenue — recurring and non-recurring. It’s vital to separate recurring and non-recurring streams into separate account bins. For example, subscriptions that automatically renew should go into their own “bin,” while non-renewing subscriptions should be kept separate. Keep services you sell under a yearly contract separate from services you sell on a one-off basis. Separating the recurring from the non-recurring helps you build projections and develop budgets more accurately.

In addition to your company’s operating revenue, you might need to account for non-operating revenue, which is income generated by activities that aren’t part of your primary line of business. Often, sources of non-operating revenue fall “below the line” on your profit and loss (P&L) statement, coming after your Net Operating Income or Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA).

Examples of non-operating revenue include:

- Commissions.

- Dividends.

- Gain on sale of assets.

- Interest income.

- Rental income.

2. Define Cost of Goods Sold and Cost of Sales

When creating a COA, people often confuse direct costs, which are costs associated with generating revenue, with indirect costs, which are connected to your business operations. One way to avoid the mix-up is to first identify your company’s direct costs, which include anything related to providing a service or delivering a product.

While your company’s direct costs might vary, the following costs typically fall under this category:

- Cost of materials

- Shipping costs

- Labor costs

- Subcontracted services costs

When determining what counts as a “direct” cost and what should be sorted into the operating expenses or indirect cost category, there are several gray areas. For example, accounting wages would fall under the operating expenses or indirect cost category at a company that sells widgets. However, at Compass East, accounting is the core function of our service and product. Therefore the wages we pay accountants and financial professionals would fall under the direct costs category.

Once you’ve identified direct costs, create separate categories for any accounts that fall under that category.

3. Identify Operating Expenses

After you’ve identified direct expenses, turn your attention to your indirect costs, also known as your operating expenses. You’re likely to have many sub-categories in this section. Expect to have several “bins” for each indirect costs sub-category.

Some examples of potential indirect costs include:

- General and administrative (G&A): Expenses connected to your overall business operation, such as the cost of insurance, utilities and rent. Any expenses related to the usual course of business used the same year they’re purchased can fall under the G&A category.

- Personnel: How much you pay your employees, particularly those who don’t have a direct connection to your company’s product or service, falls under the personnel expenses category. Benefits, bonuses and other wages fall under this category, too.

- Professional fees: If your company hires professionals, such as accountants, lawyers or consultants, group what you pay those professionals under this category. You can also include the cost of using outsourced services, such as outsourced CFOs or CIOs under the professional category.

- Fees and service charges: Any fees you pay to banks or credit card processors can fall into this sub-category.

- Technology: Some companies ground technology expenses under G&A. However, if you’re spending a lot on tech, such as software subscriptions or new hardware, it may make sense to keep technology costs separate from other administrative costs.

- Rent and Occupancy: Rent, utilities, furniture and equipment leases fall under the occupancy sub-category.

- Insurance, taxes and licenses: Your “necessary to operate” costs like insurance, business licenses, permits and operational state and local taxes can fall under this category if you decide to separate them from G&A.

- Sales and marketing expenses: What you spend to make a sale falls under the sales and marketing expenses category. It includes the cost of advertising or entertainment and meals when you’re trying to win over clients.

- Below the Line Expense: Interest you pay on debt, income taxes, penalties and fines are examples of indirect costs that fall into the non-operating expenses category.

4. Focus on the Balance Sheet

The Balance Sheet side of your COA will generally be more straightforward than the Income Statement side. Remember, there are three primary categories that fall under the Balance Sheet — Assets, Liabilities and Equity. You’ll want to create a section of the chart for each of these categories:

- Assets: Cash, fixed assets, real estate, cash equivalents and accounts receivable are all sub-categories you can include in the assets section of the COA.

- Liabilities: These accounts are for anything that your company has to pay or repay. Debt, lines of credit, wages payable and accounts payable are some sub-categories you may include here.

- Equity: Equity is what remains after you subtract business liabilities from assets. It’s your company’s value and is owned by investors, founders and employees.

5. Number Your Accounts

It’s much easier to track things down when you use a numbering system. To return to the storage facility example, you’ll be able to find the location of an item much faster if you know the shelving unit and bin number. The same is true for your accounts. To start, give each category a five-digit number. Here’s an example:

- 10000 for assets

- 20000 for liabilities

- 30000 for equity

- 40000 for operating revenue

- 50000 for costs of goods sold

- 60000 for operating expenses

- 70000 for non-operating expenses

Then you can assign a specific number to each sub-category. For example:

- Accounts related to accounts payable can start with 21000.

- Accounts under the first revenue stream can start with 41000.

- Accounts related to your company’s utilities can start with 61000.

Segmenting Your Financial Reports

Once you have the core Chart of Accounts structured, the next step is to break down the reports by classes, locations or jobs to better understand the unit economics of your business. Classes track your transactions by the meaningful segments of your business.

You can use Quickbooks to develop classes and departments. With Quickbooks, you can easily run reports and compare or use the accompanying information to develop accurate budgets for each department or class. You’ll need this information to strategize accurately. Classes also let you categorize your transactions beyond the standard account selection. If necessary, you can run individual reports to drill down into a specific department.

If you want to get insight into the profitability of a particular location, you can break down your reports by geographic area and track transactions that way. Finally, you can also segment your reports by project, which are similar to sub-customers. Using projects helps you categorize income and expenses into a specific job.

Revenue Recognition

If you have several sources of recurring revenue, such as subscription services you sell, revenue recognition accounting might be particularly useful for you when creating a COA.

Revenue recognition is an accounting principle that identifies the conditions under which you recognize revenue and account for it. It’s particularly useful if your company offers rental services or uses a subscription model.

With revenue recognition, you account for revenue on your income statement when it’s earned and realized, which, in the case of recurring revenue, might not be when you get paid. For example, if you have a contract with a customer, they might pay every month or quarter rather than paying upfront in full. Revenue recognition takes the terms of a contract into consideration.

Revenue recognition is a critical tool for accurately tracking revenue and keeping tabs on your business’ growth and performance. Using a contract management tool will also help you keep tabs on your company’s various contracts.

Compass East Can Help You Structure Your Financial Reporting

Going from the bottom up can help your company save a considerable amount of time and money in the long run. Whether you need help designing and structuring a COA or want to take advantage of our revenue recognition services, Compass East is here for you. We work to create growth strategies for our clients by providing a complete accounting and financial team, offering dynamic reporting processes and implementing technology.

We understand that each business is unique and tailor our services to meet the specific needs of each company. To learn more, contact us today.