The Bottom-Up Approach to Finance and Accounting | Data Cleanup | Building the FinOps Department | Challenge the Status Quo: The FinOps Team

We’ve identified who’s who on a traditional finance and accounting (F&A) team and have outlined some common issues with the traditional approach to F&A, such as over-reliance on a certified public accountant, manual processes and the expectation that a chief financial officer (CFO) will solve all problems. Next up is determining what your company can do to overcome these common issues.

A bottom-up approach to building the finance and accounting function has been successful in many cases. It’s so successful that we’ve established it as best practice. Learn more about taking a bottom-up approach and how your business can make it work.

The Bottom-Up Approach to Finance and Accounting

What does it mean to start at the bottom as a finance and accounting approach? It means focusing on resolving building block issues and financial infrastructure rather than perpetuating band-aid solutions. Often, the first step when taking a bottom-up approach to F&A is a Financial Operations Discovery.

Financial Operations Discovery

Admitting there is a problem is always the first step to improvement. After you’ve admitted there is a problem, the best way to untangle the identifying the underlying issues is from the viewpoint of your customers. When performing a full Financial Operations Discovery, walk through how a customer experiences your business.

Walking in your customers’ shoes lets you uncover all of the core activities of your business and discover how financial information flows through the organization. When you walk through the customer experience from marketing through financial reporting, you develop a better understanding of the systems, tools, processes and people involved in each part of your organization.

Once you know what is happening, you can work on establishing the proper infrastructure and foundation necessary to build a future-forward finance and accounting department. Without the infrastructure in place, building a scalable accounting department is impossible.

To perform your own assessment, go around the wheel asking questions about your customer. For example:

- Marketing: How do they find out about you through marketing activities? What channels are you using to reach customers? Are some channels more effective than others? Which CRM/Pipeline systems are you using to track spend and calculate customer acquisition costs?

- Sales: What is the sales and proposal process? Outbound versus inbound? How are you pricing your product or services? Are your prices competitive with others, or are you charging considerably more or less? Are these founder-led sales, or do you have a business development team in place? Are you allocating sales payroll in your customer acquisition cost calculations?

- Implementation: How are your contracts and terms structured? When customers start working with your company, do they have to commit to a certain number of purchases or a specific contract length? How does your sales team hand off a client to internal operations?

- Onboarding: What is the onboarding process with a client? What information do you need to collect from them? What is the timeline for onboarding?

- Client Service: How do you deliver your product or service? Can they renew their contract with your company? Does your account manager or client success team upsell clients? How many clients continue to work with you repeatedly?

- Technical Delivery: How does the client pay? Do you offer multiple payment options? How often are you invoicing clients?

- QA/QC: Is there someone to vet the quality of the product or service you provide? What can a client do if they have a problem with a product?

- IT: What software programs are you using, if any? Can clients use software or the internet to manage their accounts? How do you receive invoices and pay vendors or third parties?

- Accounting: How does all of this information flow to accounting? Are you closing your books on a monthly basis?

Working through this Assessment, the goal is to identify all the different ways your company generates data. Once you know where data is being generated, we can recommend the appropriate tools and systems to better capture that data. Lastly, integrating systems so they talk to one another via API creates a central source of truth for your financials. Starting at the top of the funnel and working your way through your operation will highlight all of the key touchpoints with a client and how it interacts with F&A.

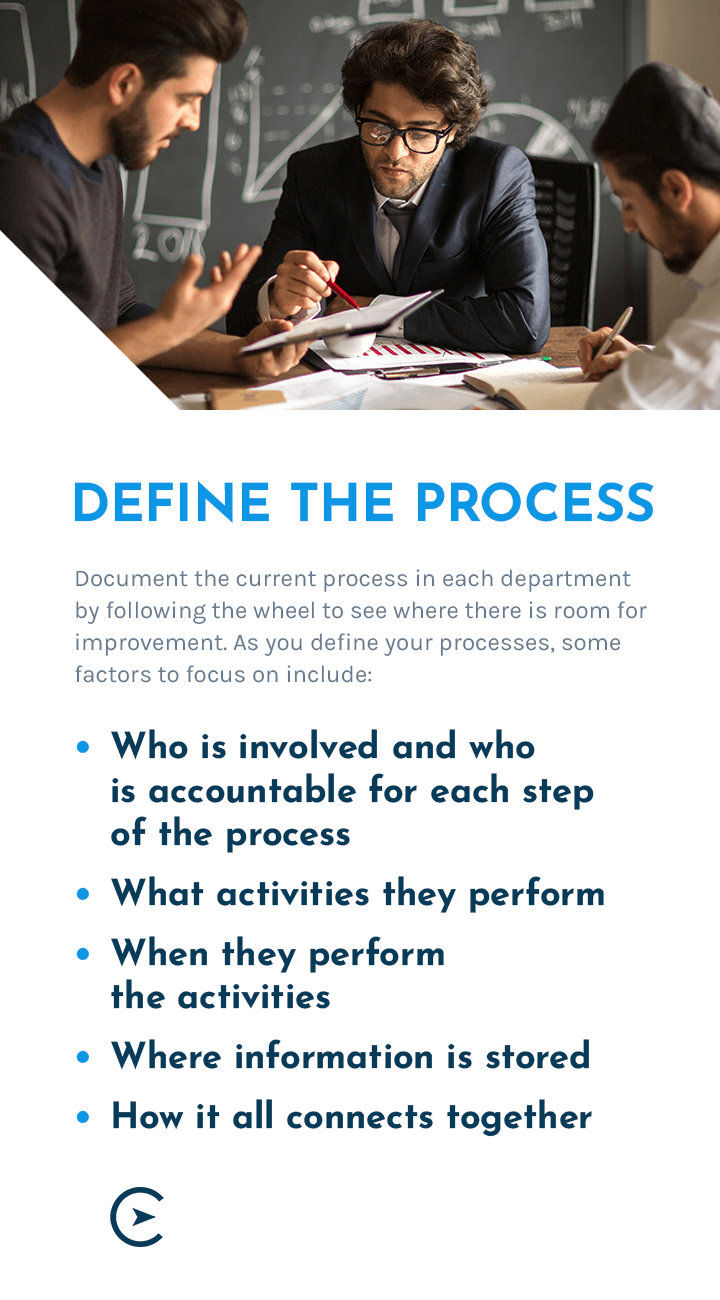

Define the Process

Document the current process in each department by following the wheel to see where there is room for improvement. As you define your processes, some factors to focus on include:

- Who is involved and who is accountable for each step of the process: What team members work in which department?

- What activities they perform: What are the responsibilities of each team member?

- When they perform the activities: At what phase of the process does a team member perform their role? What happens after they’ve completed a task? Does completing one task trigger the next one?

- Where information is stored: How does your company currently keep track of data? What technology systems, if any, do you use?

- How it all connects together: Examine the who, what, when and where to determine how everything is linked together. Once you have the basics, you can examine it more closely to discover where you can streamline the department’s process, increasing efficiency and saving money.

Data Cleanup

When you’ve completed a Financial Operations Discovery and understand what improvements are necessary to streamline the financial operation, the next step is to clean up your historical data. Bad data in equals bad data out, so it’s vital to take the actions needed to tidy things up. Your company needs accurate financials to make strategic decisions based on those financials.

Some items that often need cleanup include:

- Converting from cash to accrual: With a cash basis of accounting, your company records transactions when you get the cash for them. With an accrual basis, you record transactions when they occur, whether or not you get the cash for them. Cash basis accounting is common with smaller businesses, but as your company grows, it might switch to an accrual basis. The switch usually requires manual changes and often a complete overhaul of your accounting software program. It’s important to make sure the data is clean before moving forward.

- Establishing beginning balance sheet numbers based on the most recent tax return: Your company’s balance sheet provides an at-a-glance look at your business’s financial health. It should always balance, meaning assets should always be equal to liabilities plus equity.

- Credit card and expense recording and reconciliations: The charges on your company’s credit card statements and any other listed expenses should match those listed in your company’s ledger. Reconciling expenses and credit card statements is a must to ensure clean books.

- Fixed asset and equipment recording and reconciliations: Similarly, the recorded value of your company’s assets and equipment should align with the actual value of those assets and equipment.

- Proper revenue recognition through year-to-date: Before your company can recognize revenue, a transaction needs to take place that generates money. That can mean that revenue is recognized when the money is earned, not necessarily when your company receives it. Utilizing a contract management tool or tracker can properly align invoicing schedules and recognize revenue in the appropriate period. This is critical when building a true business health dashboard and understanding true cash flows and gross margins.

- Recording historical bills and invoices for accurate accounts payable and accounts receivable aging schedules: It’s possible for an invoice to “go missing,” meaning payment never gets recorded. The same is true for bills. Your company might have paid bills but never noted those payments. Reviewing old invoices and bills gives you the chance to correct any gaps or to track down payments for invoices.

Lastly, one of the most important aspects of any cleanup is the Chart of Accounts (COA). Your company’s COA includes the assets, liabilities and equity from the balance sheet and revenue and expenses from the balance sheet. Effectively grouping revenue streams, cost of goods sold, operating expenses and the balance sheet lets you quickly analyze financial statements and develop key performance indicators (KPIs).

Long lists of accounts don’t tell you much. When you group accounts, your company can better analyze its margins, productivity metrics, cost of customer acquisition and lifetime value of customers.

Building the FinOps Department

So far, we’ve taken a few steps on the bottom-up journey to building a future-forward finance and accounting department. Now that we’ve begun to understand the issues, put together a plan to solve them and clean up the data, we can start to focus on the development of the FinOps team.

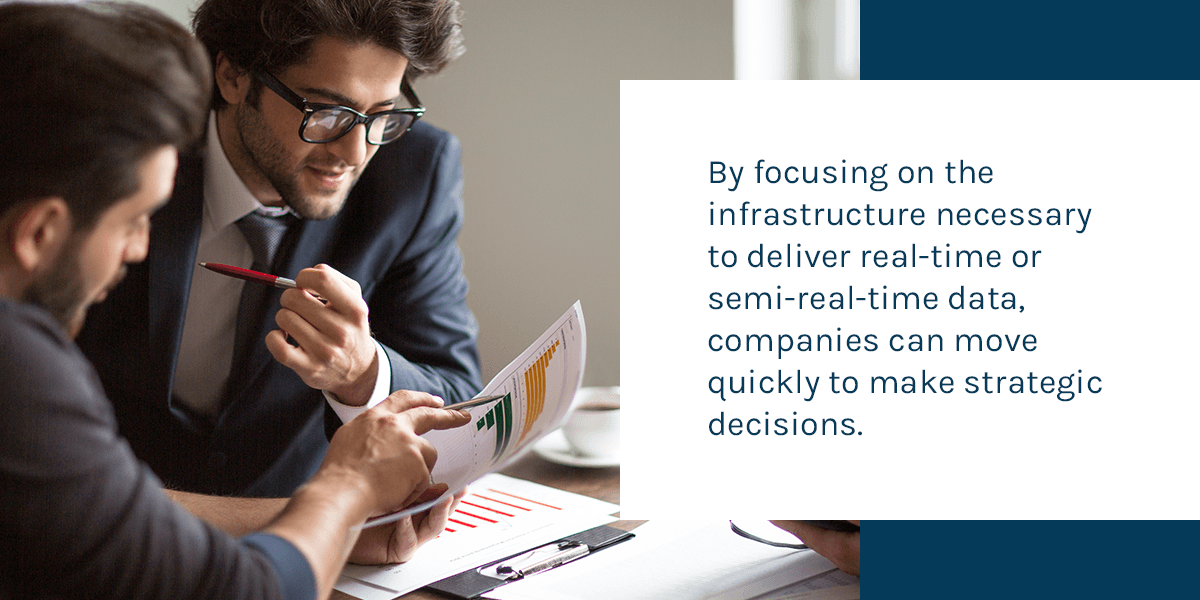

Companies today are more connected than ever, increasing the speed at which decisions are made. Cross-departmental communication is paramount. By focusing on the infrastructure necessary to deliver real-time or semi-real-time data, companies can move quickly to make strategic decisions.

It’s not just about more data, though. The ability to interpret and analyze data quickly is crucial in the new landscape. This is where the FinOps department comes in.

With a traditional finance and accounting department, the same issues tend to happen over and over. Departments can be siloed, meaning decisions and budgets are made within each department without input from the finance department. Finance and accounting has to “figure it out later” or “just make it work.”

Another issue occurs with a top-down management structure and budgeting from the CFO. The CFO often doesn’t have a clear understanding of the company’s day-to-day activities or pain points. They often create unrealistic expectations or make budget cuts, which can hurt innovation and morale. A FinOps team alleviates these issues.

The FinOps team is interconnected with a company. The team has fluidity across departments, allowing them to leverage technology infrastructure and operational and financial KPIs, to understand what is happening on a granular level. The team’s interconnectivity means they can analyze information in real time.

When you build your finance department with a FinOps mindset, you unsilo information and give finance and accounting the chance to help with strategic decision-making. The team brings an objective viewpoint based on financial data, allowing various departments to make critical decisions. Ultimately, communication increases across departments. The company’s operations become more transparent, and each department becomes more accountable.

The roles and backgrounds of the FinOps team start with technology at their core.

Challenge the Status Quo: The FinOps Team

Who’s who on a FinOps team? Take a look at the various roles and what those roles mean.

Accounting Technologist Role Definition

In the traditional accounting department, bookkeepers and staff accountants keep the books, code bills and maintain the general ledger, among other tasks. They’re valued for their knowledge of accounting and are generally optimized for specific activities.

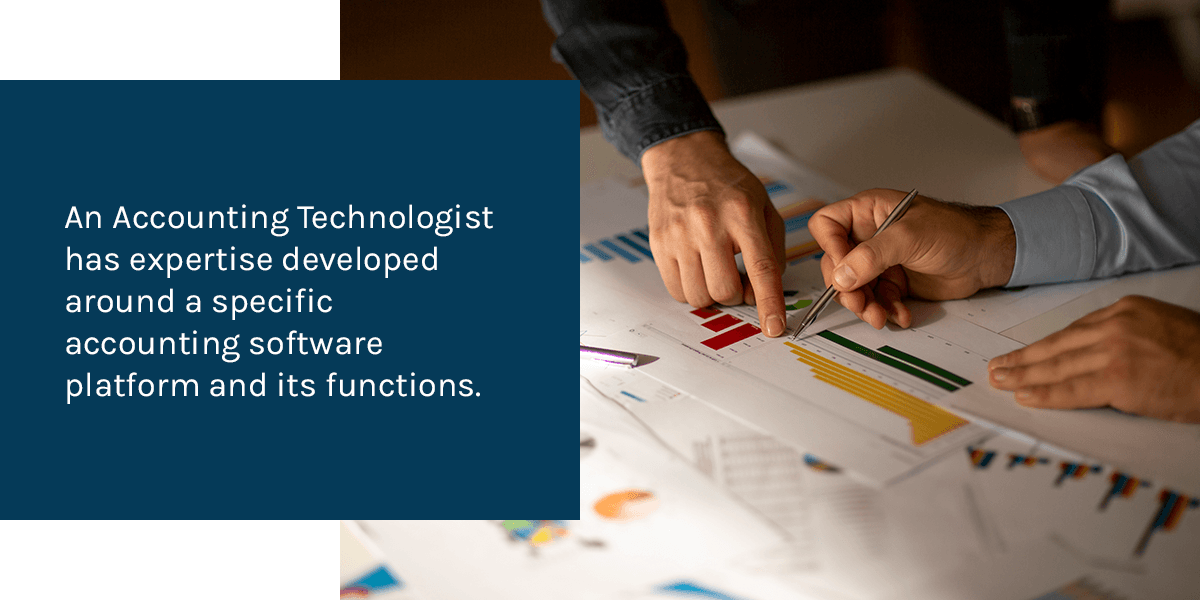

The increased prevalence of software programs means some of the traditional accounting responsibilities have been automated or eliminated. Today, rather than an all-in-one enterprise resource planning (ERP) solution, flexible accounting software is being developed at a rapid pace. Each software program has a specified function. As the need for traditional bookkeepers and accountants to manage various technology systems has grown, the skill set has also evolved giving rise to the Accounting Technologist. An Accounting Technologist has expertise developed around a specific accounting software platform and its functions, utilizes automation when available to make them more efficient, and understands how each system connects with one another.

Controller Role Definition

Traditionally, the Controller is the person in charge of a company’s finances. Just as the traditional accountant roles have evolved, so has the Controller’s role. The Controller still serves as the final review point for developing accurate financials and needs to be fluent in the technology systems and tools a company uses. They need to be able to properly develop and track the lagging financial KPIs of the business and have a deep understanding of what happened last month to inform decision-makers and update budgets.

Financial Technologist Role Definition

The Financial Analyst spends their day developing Excel models for the CFO and Finance Planning & Analysis (FP&A) department. Their role traditionally required a lot of manual model building and rebuilding. A Financial Analyst might spend many hours building models, which often have a tendency to break when they are unwieldy. They also traditionally pull and update KPIs manually.

On the FinOps team, the Financial Analyst evolves into the Financial Technologist, who has many of the same skill sets as a Financial Analyst. The difference is the tools they use.

A Financial Technologist uses KPI Dashboards, Business Intelligence and Analytic tools, Cash Forecasts and Financial models that are built into specific software platforms. The software integrates with the general ledger, so there’s no need to import or export information or make updates in Excel. Instead, the Financial Technologist builds the models into software tools and maintains them inside the system. The role requires a high level of expertise. As the FinOps department evolves, the Financial Technologist role becomes much more specialized and focused on data analytics and business intelligence visualizations.

Financial Strategist Role Definition

Historically, CFO’s have a banking background and expertise in raising money. They also excel at mergers and acquisitions and developing complex debt structures. The CFO is also traditionally the gatekeeper and decision-maker. They tell departments “no” based on budgets or if there’s a need to reduce costs based on a top-down approach. They are still a key decision-maker at the top of the finance and accounting department and fill the strategic, forward-looking need for high-growth companies.

The CFO role is evolving into the role of Financial Strategist. A Financial Strategist leverages technology, connecting historical financial data with a company’s forward-focused strategy. They know the numbers and can tell the growth story. They are an active participant in strategy conversations and management discussions. The Financial Strategist has financial knowledge at their fingertips that allows them to support company decisions. They also use technology to analyze complex data sources, breaking the data down into actionable insights and providing the information the team needs to make decisions.

Compass East Can Help Your Company Build Its FinOps Team From the Bottom Up

If your company is ready to build Finance and Accounting from the bottom up, Compass East can help. We help companies in many industries grow and improve. We’ve developed technological systems that streamline processes and ensure companies remain in compliance with regulation and accounting principles. Contact us today to learn more about how we’ll use technology to build your FinOps Team from the bottom up.

Our Finance and Accounting Technology Stack